All Categories

Featured

Table of Contents

A PUAR enables you to "overfund" your insurance plan right as much as line of it coming to be a Changed Endowment Agreement (MEC). When you utilize a PUAR, you quickly enhance your cash money value (and your fatality benefit), therefore raising the power of your "bank". Further, the more cash money value you have, the better your passion and returns settlements from your insurance policy company will certainly be.

With the increase of TikTok as an information-sharing system, economic advice and approaches have actually found a novel method of dispersing. One such method that has been making the rounds is the unlimited financial concept, or IBC for short, gathering endorsements from stars like rap artist Waka Flocka Flame. However, while the technique is currently preferred, its roots trace back to the 1980s when financial expert Nelson Nash presented it to the globe.

What are the common mistakes people make with Infinite Banking Wealth Strategy?

Within these plans, the money value expands based on a price set by the insurance firm (Bank on yourself). Once a considerable cash money worth accumulates, insurance holders can get a cash money worth car loan. These lendings differ from traditional ones, with life insurance policy functioning as collateral, implying one can lose their protection if loaning excessively without adequate money worth to sustain the insurance coverage costs

And while the attraction of these plans is apparent, there are innate constraints and threats, necessitating thorough cash money worth surveillance. The approach's legitimacy isn't black and white. For high-net-worth people or company owners, especially those making use of strategies like company-owned life insurance policy (COLI), the benefits of tax obligation breaks and substance development can be appealing.

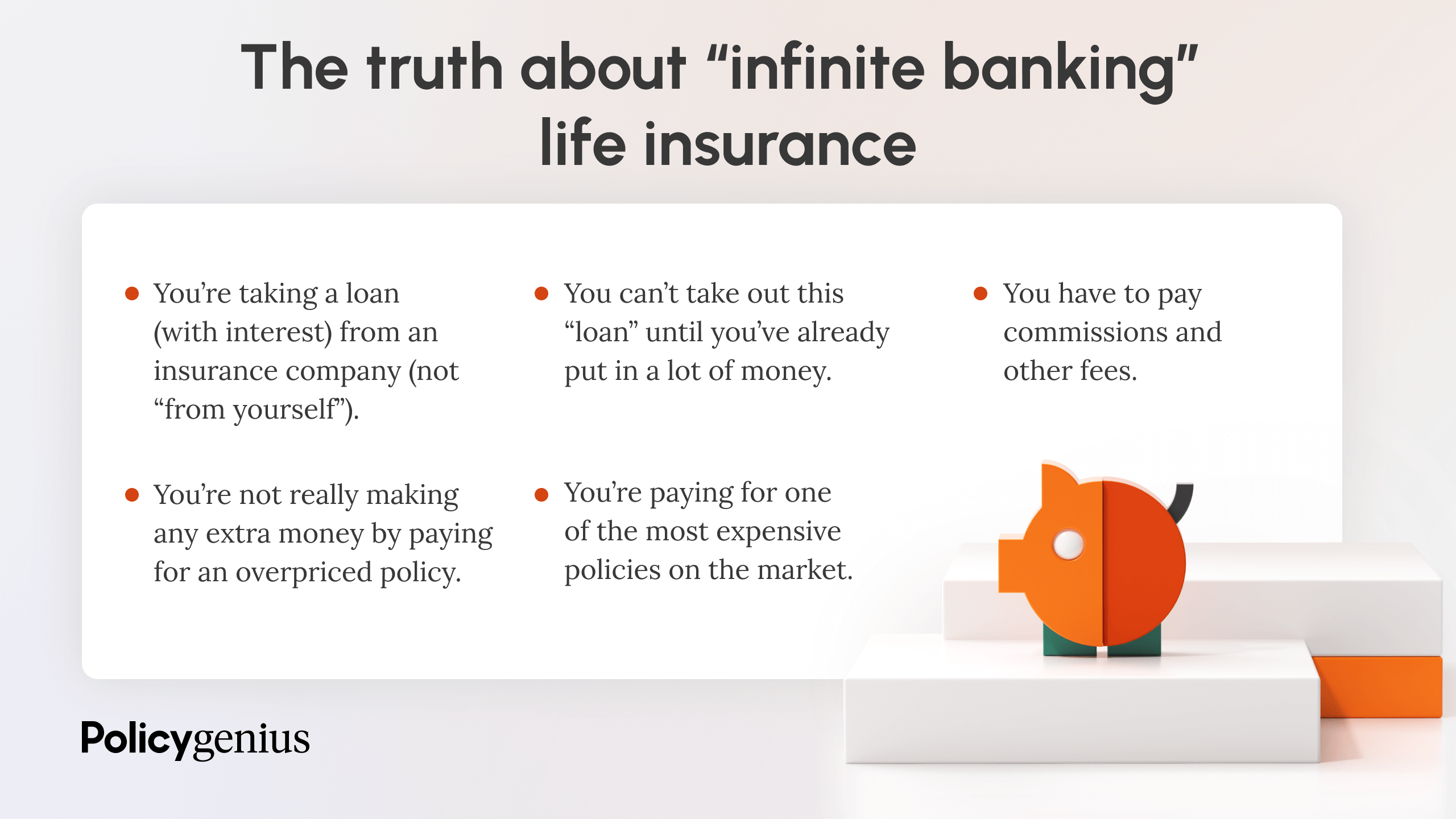

The allure of unlimited financial does not negate its challenges: Cost: The foundational requirement, a long-term life insurance coverage policy, is more expensive than its term equivalents. Qualification: Not everyone gets approved for whole life insurance policy due to strenuous underwriting processes that can leave out those with particular health and wellness or way of life conditions. Intricacy and danger: The intricate nature of IBC, coupled with its threats, may hinder several, especially when simpler and less high-risk choices are available.

Can I use Policy Loan Strategy to fund large purchases?

Alloting around 10% of your monthly revenue to the plan is simply not possible for most individuals. Part of what you read below is merely a reiteration of what has actually already been stated above.

Prior to you obtain yourself into a scenario you're not prepared for, understand the complying with first: Although the idea is frequently sold as such, you're not really taking a lending from on your own. If that held true, you wouldn't need to repay it. Rather, you're obtaining from the insurer and need to settle it with passion.

Some social media messages advise using money worth from whole life insurance coverage to pay down credit scores card financial debt. When you pay back the lending, a portion of that rate of interest goes to the insurance coverage company.

For the very first a number of years, you'll be paying off the commission. This makes it extremely tough for your plan to build up value throughout this time. Unless you can pay for to pay a couple of to a number of hundred bucks for the following decade or more, IBC won't function for you.

Generational Wealth With Infinite Banking

If you call for life insurance, here are some valuable tips to take into consideration: Consider term life insurance coverage. Make sure to go shopping around for the ideal rate.

Picture never ever needing to stress over financial institution car loans or high rate of interest again. What if you could borrow money on your terms and construct wide range concurrently? That's the power of boundless banking life insurance policy. By leveraging the cash money worth of whole life insurance policy IUL policies, you can grow your wide range and obtain cash without counting on traditional financial institutions.

There's no set funding term, and you have the freedom to select the repayment timetable, which can be as leisurely as paying off the financing at the time of death. Whole life for Infinite Banking. This versatility prolongs to the maintenance of the car loans, where you can go with interest-only settlements, keeping the loan equilibrium level and manageable

Holding cash in an IUL taken care of account being attributed interest can often be far better than holding the cash money on down payment at a bank.: You have actually always desired for opening your own bakery. You can obtain from your IUL plan to cover the preliminary costs of renting out an area, acquiring tools, and employing team.

Is there a way to automate Whole Life For Infinite Banking transactions?

Personal finances can be acquired from conventional banks and credit rating unions. Borrowing money on a credit history card is usually really expensive with yearly percentage prices of interest (APR) often reaching 20% to 30% or more a year.

{kind=link}

Latest Posts

Be Your Own Bank Through Bitcoin Self-custody

Be My Own Bank

Bank Account Options For Kids, Teens, Students & Young ...